Foreigners can apply for a mortgage at Mizuho Bank if they meet the bank’s specific residency and income requirements.

You will find the process more manageable when you understand the documents, screening steps, and conditions involved.

This guide explains everything you need to prepare before submitting your application.

Basic Requirements for Foreigners

You need to meet several basic conditions before Mizuho Bank reviews your mortgage application.

These requirements help the bank confirm your stability and residency status in Japan. Knowing them early saves you time and prevents delays.

- Valid residence status (long-term, work visa, or permanent residency)

- Stable monthly income from a Japan-based employer

- At least one to two years of employment history in Japan

- Proof of taxes paid in Japan (tax certificate or income certificate)

- Passport and residence card

- Japanese bank account with a consistent transaction history

- Contact information and the current registered address in Japan

Mizuho Bank Eligibility Conditions

Mizuho Bank follows clear criteria to confirm if you qualify for a mortgage. You must meet these conditions before they continue the review.

These checks help the bank assess your stability in Japan.

- Accepted visa types include permanent residency, long-term work visas, or highly skilled professional visas.

- Applicant age must fit within the bank’s borrowing range, usually up to around 65–70 years old at loan maturity.

- Stable and verifiable employment in Japan with regular monthly income.

- The maximum loan-to-value (LTV) ratio is set by the bank, typically allowing financing up to a specified percentage of the property’s price.

- Ability to meet repayment terms based on income, debts, and financial history.

- Sufficient credit history or financial record in Japan.

- Property must meet Mizuho’s appraisal standards and legal requirements.

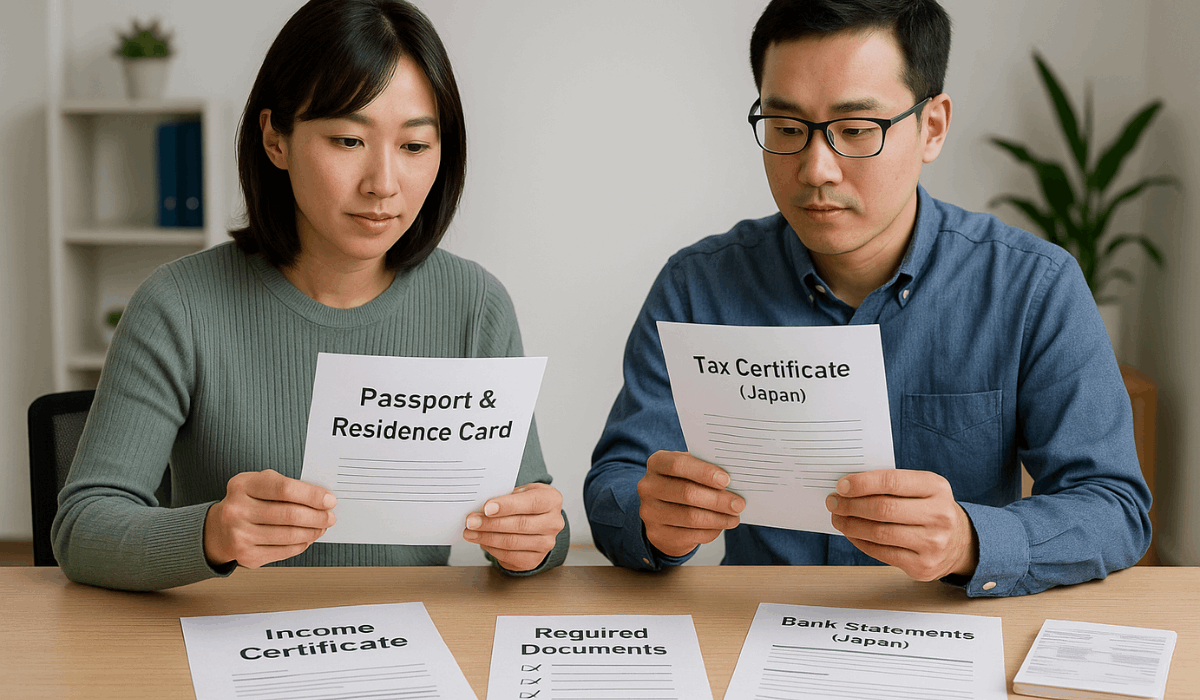

Required Documents

You need to prepare several documents before Mizuho Bank reviews your mortgage application.

These papers confirm your identity, income, and eligibility. Having them ready helps you avoid delays during screening.

- Passport and residence card

- Certificate of income or tax certificate issued in Japan

- Employment contract or recent pay slips

- Bank statements from your Japanese bank account

- Proof of address, such as a utility bill or residence registration

- Property information, including floor plans and seller details

- Documents related to the down payment, such as savings proof

- Any translated documents, if the bank requests them

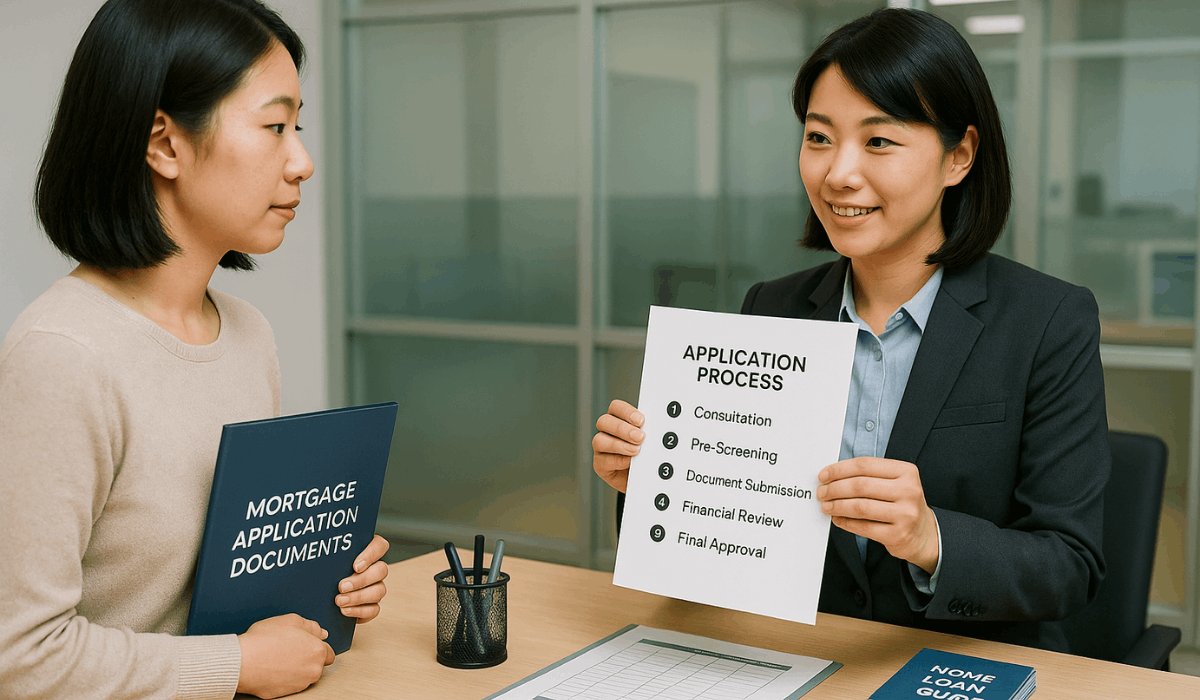

How the Application Process Works

The mortgage application at Mizuho Bank follows a structured process.

You will move through each step as the bank checks your documents and financial stability. Knowing the flow helps you prepare in advance.

- Consultation: Your first meeting with the bank to ask questions and confirm basic eligibility.

- Pre-screening: A quick financial check to see if you meet the minimum requirements.

- Document Submission: You hand in all required papers for verification.

- Financial Assessment: The bank reviews your income, debts, and credit record.

- Provisional Decision: Mizuho gives you an initial approval or requests more information.

- Property Review: The bank checks the property details, value, and legal status.

- Contract Signing: You sign the official mortgage agreement after final approval.

- Loan Disbursement: Mizuho releases the funds to complete the property purchase.

Interest Rates and Mortgage Types

Mizuho Bank offers several mortgage types with clear rate structures. You must know how each one works before choosing.

These options affect your monthly and total repayment costs.

- Floating Rate: Interest changes based on Mizuho’s variable rate. Monthly payments can rise or fall every review period.

- Fixed Rate: Rate stays the same for a set period (2, 3, 5, 10 years). Payments remain stable during that fixed term.

- Full-Term Fixed: One fixed rate for the entire loan period. Monthly payments never change.

- Combination Mortgage: The Loan is split between fixed and floating. Part stays stable, part adjusts with the market.

- Discounted Rate Plan: Lower interest rate during the first years of the loan. After the discount period, the rate switches to Mizuho’s standard fixed or floating rate.

Credit Review and Risk Evaluation

Mizuho Bank reviews your financial background to confirm you can repay the mortgage.

The bank checks your income stability, credit history, and existing debts. These steps help determine your overall risk level as a borrower.

- Income Stability Check: Mizuho confirms your monthly salary, employer type, and length of employment.

- Credit History Review: The bank checks your payment record in Japan, including past loans, credit cards, and missed payments.

- Debt-to-Income Ratio: Mizuho calculates how much of your income already goes to other debts to ensure you can handle a new loan.

- Savings and Assets: The bank reviews your savings balance, down payment funds, and overall financial reserves.

- Visa and Residency Status: Longer or permanent residency reduces perceived risk by demonstrating long-term stability in Japan.

- Employment Type: Full-time employees are evaluated more favorably than contract or part-time workers due to the reliability of income.

- Property Assessment: The bank assesses the property’s market value and legal status to confirm it’s safe and sound collateral.

Additional Costs to Prepare For

A mortgage from Mizuho Bank comes with several extra costs beyond the loan itself.

You need to budget for these expenses before signing the contract. Preparing early helps you avoid surprises during the final approval.

- Administrative Fees: Charges for processing your loan application and issuing the mortgage documents.

- Stamp Duty: A government tax required for official loan agreements.

- Registration Fees: Costs for registering the property and the mortgage with the relevant authorities.

- Fire and Earthquake Insurance: Mandatory coverage required for all financed properties in Japan.

- Loan Guarantee Fee: A fee paid to a guarantor company if required by the bank.

- Notary or Legal Service Costs: Fees for document preparation, confirmations, and legal checks.

- Property Appraisal Fee: Charges for evaluating the property’s market value.

- Taxes on Property Purchase: Includes acquisition tax and potential municipal transfer taxes.

Tips for Foreign Applicants

Foreign applicants face extra steps when applying for a mortgage in Japan.

You can make the process smoother by preparing early and avoiding common mistakes. These tips help you meet the bank’s expectations more easily.

- Keep your residency status valid: Ensure your visa has sufficient time remaining when you apply.

- Prepare translated documents: Provide official translations if any document is not in Japanese.

- Maintain stable employment: Stay with the same employer before and during the application.

- Build a clean credit record: Pay all bills, cards, and loans on time to avoid any negative marks.

- Increase your savings: A stronger down payment improves approval chances.

- Avoid major purchases: Do not take on new loans or incur significant expenses before approval.

- Use bilingual support: Choose a branch or loan officer who offers English assistance.

- Confirm property details early: Make sure the property meets legal and appraisal requirements.

- Organize all documents: Ensure all required papers are up to date and ready for submission.

Contact Information

You can reach out to Mizuho Bank to ask about the mortgage process, set up a meeting, or request English support.

Use the details below to connect with them directly.

- Toll-free in Japan (English service available): 0120-324-638

- Head office address: Otemachi Tower, 1-5-5 Otemachi, Chiyoda-ku, Tokyo 100-8176, Japan

- General phone number at head office: +81-3-3214-1111

To Sum Up

Getting a mortgage from Mizuho Bank is easier when you understand the requirements, documents, and screening steps.

You now have the key details you need to prepare confidently as a foreign applicant in Japan.

Start your application today by contacting Mizuho Bank and confirming your eligibility.

Disclaimer

This guide is for general information only and may not reflect the latest updates from Mizuho Bank.

Always confirm current requirements, rates, and conditions directly with the bank before submitting any application.